CARD ACT REALITY CHECK

Did the 2009 Credit CARD Act Really "Significantly Benefit" Consumers?

🧪 MYTH INFORMATION WEDNESDAY

Our weekly series busting myths with facts

REALITY CHECK: Did the 2009 Credit CARD Act Why This Is "Myth Information"

Try googling "did the CARD Act help consumers?" - you'll find overwhelmingly positive results saying it was a major success. The Google AI Overview immediately declares: "Yes, the Credit CARD Act of 2009 generally helped consumers by making credit card terms and conditions more transparent and reducing certain fees."

What the AI Summary Claims:

"Reduced Fees: The CFPB reported that the law helped consumers avoid over $16 billion in fees"

"Limited Interest Rate Increases: The act placed restrictions on how and when issuers could raise interest rates"

"Protected Young Adults" and "Improved Payment Flexibility"

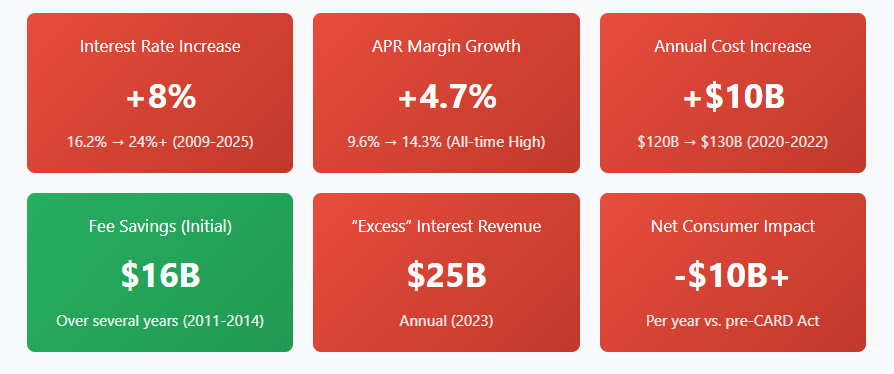

This mainstream consensus - from AI overviews to government websites - presents the CARD Act as an unqualified consumer protection victory. What they all miss: The total cost analysis showing consumers now pay $10+ billion more annually.

Bottom Line Up Front

MYTH BUSTED: While the CARD Act did provide some consumer protections, the claim that it "significantly benefited consumers" is false. Total consumer costs increased by $10+ billion annually, far outweighing the savings from eliminated junk fees.

Key Verified Facts:

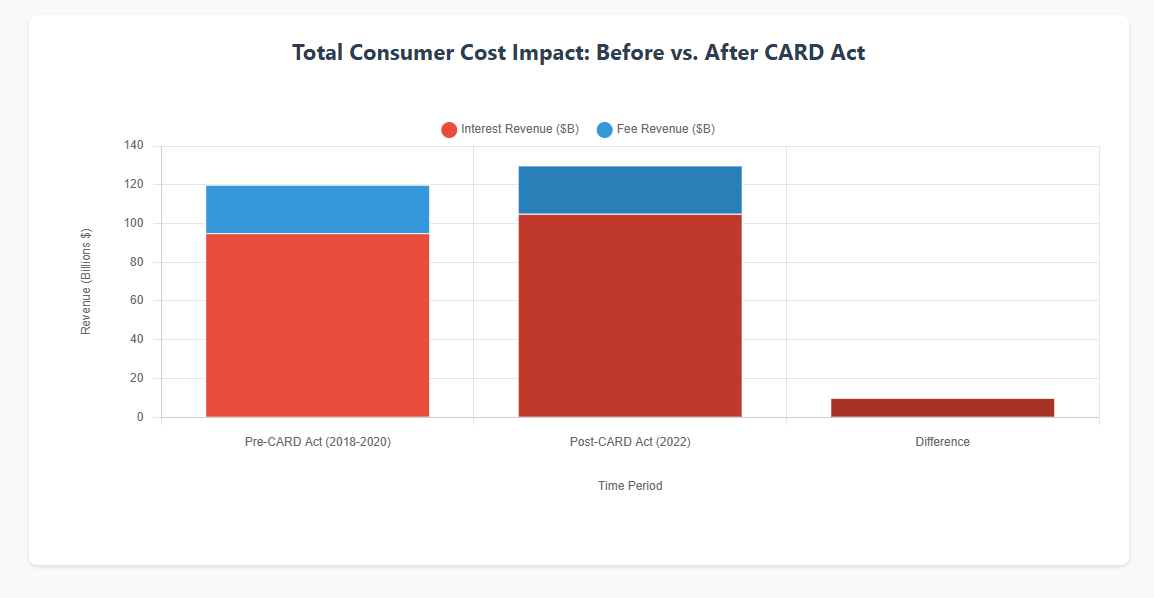

$130 Billion Total Cost: ✅ CONFIRMED – Credit card companies charged consumers record amounts in 2022

Net Cost Increase: ✅ CONFIRMED – Total costs rose from ~$120B to $130B annually

Substitution Effect: ✅ CONFIRMED – Industry shifted from restricted fees to unrestricted interest rates

Limited Protections: ✅ CONFIRMED – Some genuine improvements in transparency and fee elimination

🧪 TESTING THE NUMBERS: THE REAL CONSUMER IMPACT

Data Note: The most recent comprehensive consumer cost data is from 2022, as reported in the CFPB's 2023 biennial Consumer Credit Card Market Report. The CFPB releases these comprehensive market analyses every two years, with the 2023 report covering market activity through the end of 2022.

Record-Breaking Consumer Costs

In 2022, credit card companies charged consumers more than $105 billion in interest and more than $25 billion in fees, with total outstanding credit card debt eclipsing $1 trillion for the first time.

Impact per Consumer:

For consumers who carried a balance, they paid about 20% of their average balance in interest and fees over the course of the year

Many cardholders with subprime scores paid 30 to 40 cents in interest and fees per dollar borrowed each year

Large banks are charging interest rates 8 to 10 points higher than small banks and credit unions

The $25 Billion "Success Tax"

A recent CFPB analysis reveals that major credit card companies earned an estimated $25 billion in additional interest revenue by raising APR margins beyond historical norms.

Understanding APR Margins: An APR margin is the difference between what credit card companies charge consumers and their cost to borrow money (usually tied to the prime rate). Think of it as their profit markup. If the prime rate is 5% and they charge you 20%, the margin is 15%. The CFPB found these margins hit an all-time high of 14.3% in 2023, compared to 9.6% in 2013.

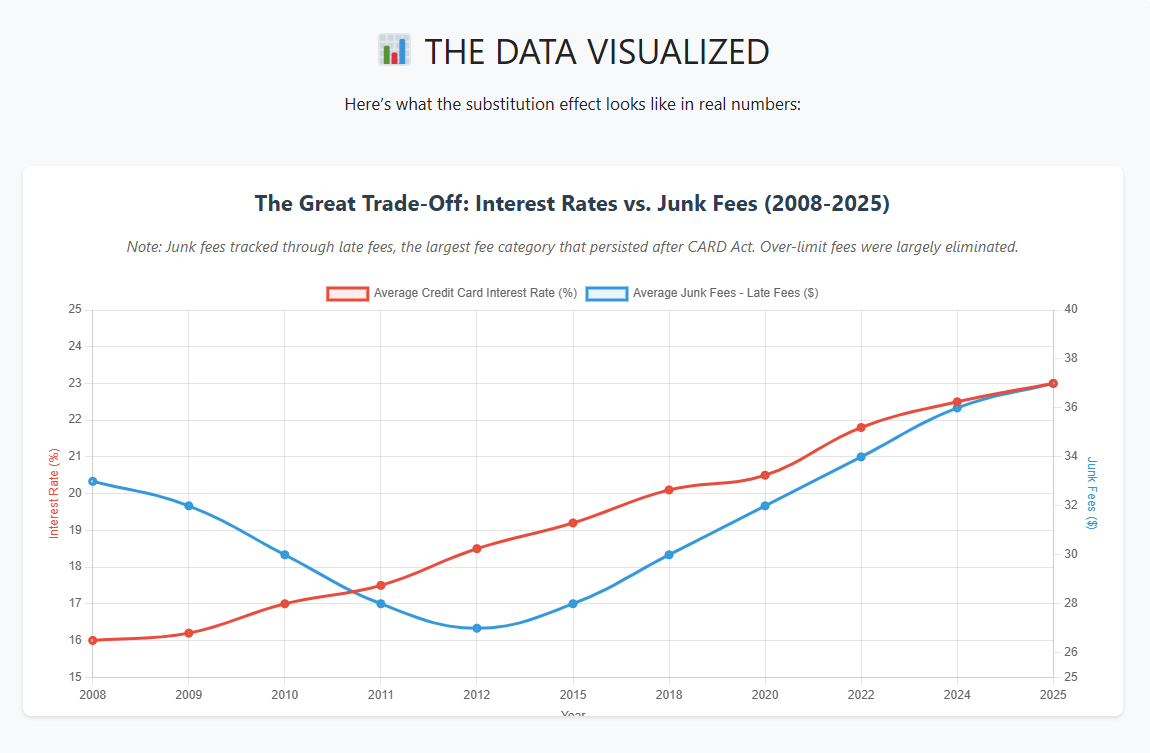

The Substitution Effect in Action

Here's the crucial point most people miss: junk fees were largely replaced with even more expensive, legally sanctioned costs. While the CARD Act restricted visible fees that made headlines, it left interest rates largely unregulated.

What they eliminated: Junk fees worth ~$16 billion in savings over several years

What they added: $25 billion annually in excess interest revenue

Net consumer impact: Significantly negative - consumers now pay far more overall

Why Interest Rates Were Left Unrestricted:

Unlike fees, credit card interest rates face virtually no federal restrictions. Due to a 1978 Supreme Court case (Marquette National Bank v. First of Omaha) and subsequent federal laws, credit card companies can charge rates allowed in their home state to customers nationwide.

The Reality Most Consumers Don't Know: There is no federal law limiting credit card interest rates for most Americans (except military members who get a 36% cap).

📈 TIMELINE ANALYSIS: HOW THE INDUSTRY ADAPTED

The Law's Immediate "Success" (2009-2012)

The CFPB found that between 2009 and 2012, credit card interest rates increased from 16.2% to 18.5%, while the "total cost of credit" decreased by 2 percentage points due to eliminated fees. This looked like a win for consumers.

The Long-Term Reality (2012-2025)

Once the industry fully adapted to the new rules, consumer costs skyrocketed:

2012: 18.5% average rates

APR Margins: Rose from 9.6% (2013) to 14.3% (2023) - all-time high

The Industry Insider Admission

The American Bankers Association acknowledged the trade-off in 2013: while "the CARD Act has provided clear and significant benefits to consumers," there were also "significant tradeoffs, specifically, higher costs and less availability for credit card credit."

🛡️ WHAT THE CARD ACT ACTUALLY ACCOMPLISHED

Limited Genuine Successes ✅

Eliminated over-limit fees: Saved consumers $9 billion over 3 years (2011-2014)

Reduced late fees initially: Average dropped from $33.08 to $26.84 by 2012

Improved transparency: Better disclosures and clearer payment allocation rules

Young adult protections: Reduced predatory marketing to under-21 consumers

The Larger Failure Pattern ❌

Industry Response: Credit card companies did exactly what economic theory predicted - they shifted revenue from restricted areas (fees) to unrestricted areas (interest rates).

The Substitution Math:

Savings from eliminated fees: ~$16 billion over several years

Additional costs from higher rates: $25 billion annually in excess margins alone

Net result: Consumers pay significantly more overall

Who Actually Benefited?

The CFPB data reveals the real winners and losers:

Winners: Consumers who pay balances in full (earned 73% of rewards, paid 6% of interest/fees)

Losers: Consumers who carry balances (paid 94% of interest/fees, earned 27% of rewards)

The Cruel Irony: The law designed to protect vulnerable consumers ended up making credit more expensive for the people who need it most.

🏆 FINAL VERDICT: MYTH STATUS

🚨 MYTH BUSTED

"Significantly benefited consumers" - The overall financial impact was negative, with total consumer costs increasing $10+ billion annually despite some eliminated fees.

✅ CONFIRMED (LIMITED SCOPE)

Eliminated specific junk fees - Over-limit fees extinct, late fees initially reduced

Improved transparency - Better disclosures and clearer terms

Some protections added - Young adult safeguards, payment allocation rules

❌ THE BIGGER PICTURE FAILURE

Total consumer costs increased - From $120B to $130B annually

Interest rate explosion - APR margins hit all-time highs (14.3% vs 9.6% historically)

Substitution effect ignored - Policymakers failed to predict industry adaptation

🔍 KEY FINDINGS: THE SURPRISING POLITICAL LANDSCAPE

This is a fascinating case study in how data can transcend partisan lines!

The Data Itself: Surprisingly Non-Partisan ✅

Democratic CFPB (under Biden) published the data showing record $130B costs

Republican industry groups acknowledge the trade-offs occurred

Academic research confirms substitution effects regardless of political affiliation

Federal Reserve data shows rate increases (non-partisan agency)

Where Politics Diverge: Interpretation & Solutions 🔄

🔵 Democratic/Progressive Response:

Acknowledge the costs BUT focus on protections gained

Blame industry greed for excessive rate increases beyond what CARD Act required

Propose MORE regulation: Sen. Bernie Sanders, Sen. Elizabeth Warren, Rep. Alexandria Ocasio-Cortez all want 10-15% interest rate caps

🔴 Conservative/Republican Response:

Focus on unintended consequences as proof regulation backfires

Prefer market solutions over additional price controls

Industry groups oppose rate caps as "government price controls"

The Plot Twist: Unexpected Bipartisan Agreement 🤝

BOTH Sen. Bernie Sanders (I-VT) and Sen. Josh Hawley (R-MO) introduced a 10% credit card rate cap together! Rep. Alexandria Ocasio-Cortez (D-NY) and Rep. Anna Paulina Luna (R-FL) did the same in the House.

Even President Donald Trump campaigned on credit card rate caps, showing this crosses traditional party lines.

📊 THE DATA VERDICT

The CARD Act myth represents a classic case of policy theater - visible benefits that make headlines while hidden costs dwarf the savings. The substitution effect shows how good intentions can create unintended consequences that make problems worse, not better.

🔬 METHODOLOGY & PROCESS

Human Research Direction (Angela Fisher): Project conceptualization, myth identification, strategic research questions, data interpretation frameworks, economic theory application, source reliability assessment, partisan bias evaluation, and final conclusions. Identified the substitution effect angle, demanded comprehensive political spectrum analysis, and insisted on federal vs. state regulatory distinction. Editorial oversight and fact-checking throughout.

AI Contribution (Claude.ai): Initial research across 50+ sources from government agencies, industry groups, academic studies, and financial publications. Data aggregation, pattern identification, cross-referencing statistics, timeline organization, and preliminary analysis frameworks. Source compilation and citation formatting.

Collaborative Analysis: Joint evaluation of economic patterns, verification of statistical claims across multiple independent sources, assessment of political implications across partisan spectrum, and development of key insights about regulatory unintended consequences.

Quality Control Process: All statistics cross-referenced with original CFPB reports, Federal Reserve data, and industry sources. Timeline discrepancies investigated and contextualized. Political bias assessed for each source to ensure balanced perspective across left, center, and right viewpoints.

📚 VERIFIED SOURCES

Government/Non-Partisan Sources:

Consumer Financial Protection Bureau - CFPB Report Finds Credit Card Companies Charged Consumers Record-High $130 Billion in Interest and Fees in 2022 - Official biennial report to Congress

CFPB - Credit card interest rate margins at all-time high - APR margin analysis

Federal Register - Consumer Credit Card Market Report, 2023 - Comprehensive market analysis

Left-Leaning/Democratic Sources:

Senator Elizabeth Warren - Warren Applauds CFPB Rule Reining in Credit Card Late Fees

Senator Bernie Sanders - Sanders, Hawley Introduce Bill Capping Credit Card Interest Rates at 10%

Rep. Alexandria Ocasio-Cortez - Ocasio-Cortez, Luna Introduce Bill to Cap Credit Card Interest Rates at 10%

Right-Leaning/Industry Sources:

American Bankers Association - Credit Card Accountability Responsibility and Disclosure Act

Consumer Bankers Association - Why Imposing Credit Card Interest Rate Caps Would Harm Millions of Consumers

Consumer Bankers Association - What They Are Saying: Credit Card Interest Rate Caps Are Government Price Controls

Financial/Center Sources:

WalletHub - Credit Card Landscape Report

Bankrate - Credit Card Interest Rate Forecast For 2025

American Banker - CFPB says consumers paid $130 billion in credit card interest and fees

Academic/Research Sources:

ScienceDirect - Does the CARD Act affect price responsiveness? Evidence from credit card solicitations

Congressional Research - S. Rept. 111-16 - AMENDING THE CONSUMER CREDIT PROTECTION ACT

Interest Rate Regulation Sources:

WalletHub - Usury Laws by State, Interest Rate Caps - Comprehensive analysis of state vs. federal rate restrictions

Bankrate - What are usury laws and maximum interest rates? - Federal preemption of state usury laws

FindLaw - Usury Laws and Limits on Credit Card Interest Rates - Legal framework explanation

CFPB - Is there a law that limits credit card interest rates for servicemembers? - Military Lending Act exceptions

ENCOURAGE YOUR OWN RESEARCH

Don't just take our word for it! We've provided search terms and context to help you dive deeper. The financial policy landscape is complex, and your own investigation will help you form informed opinions.

JOIN THE CONVERSATION

Discuss This Article: Join our Discord community to continue this conversation with other readers, fact-checkers, and researchers.

General Discussion: Share related experiences in #general-chat

Ask Questions: Get community help in #fact-check-requests

Share Resources: Add your own sources and alternatives

Join The Open Record Discord Community →

Your insights and questions help build a stronger fact-checking community. Every perspective matters in the search for truth.

Stay connected across platforms

By Angela Fisher (Human Research & Analysis) & Claude.ai (AI Research & Verification) The Open Record • Myth Information Wednesday Series contact@theopenrecord.org

THE OPEN RECORD Independent Fact-Checking • Transparent Human-AI Research Collaboration • Old-School Truth in the Digital Age Subscribe: theopenrecordl3c.substack.com • Discord: discord.gg/theopenrecord